Why are cocoa prices still going up – and what does it mean?

Cocoa prices are still skyrocketing. We are going to do a deep dive to try and answer a few key questions.

Print / PDF

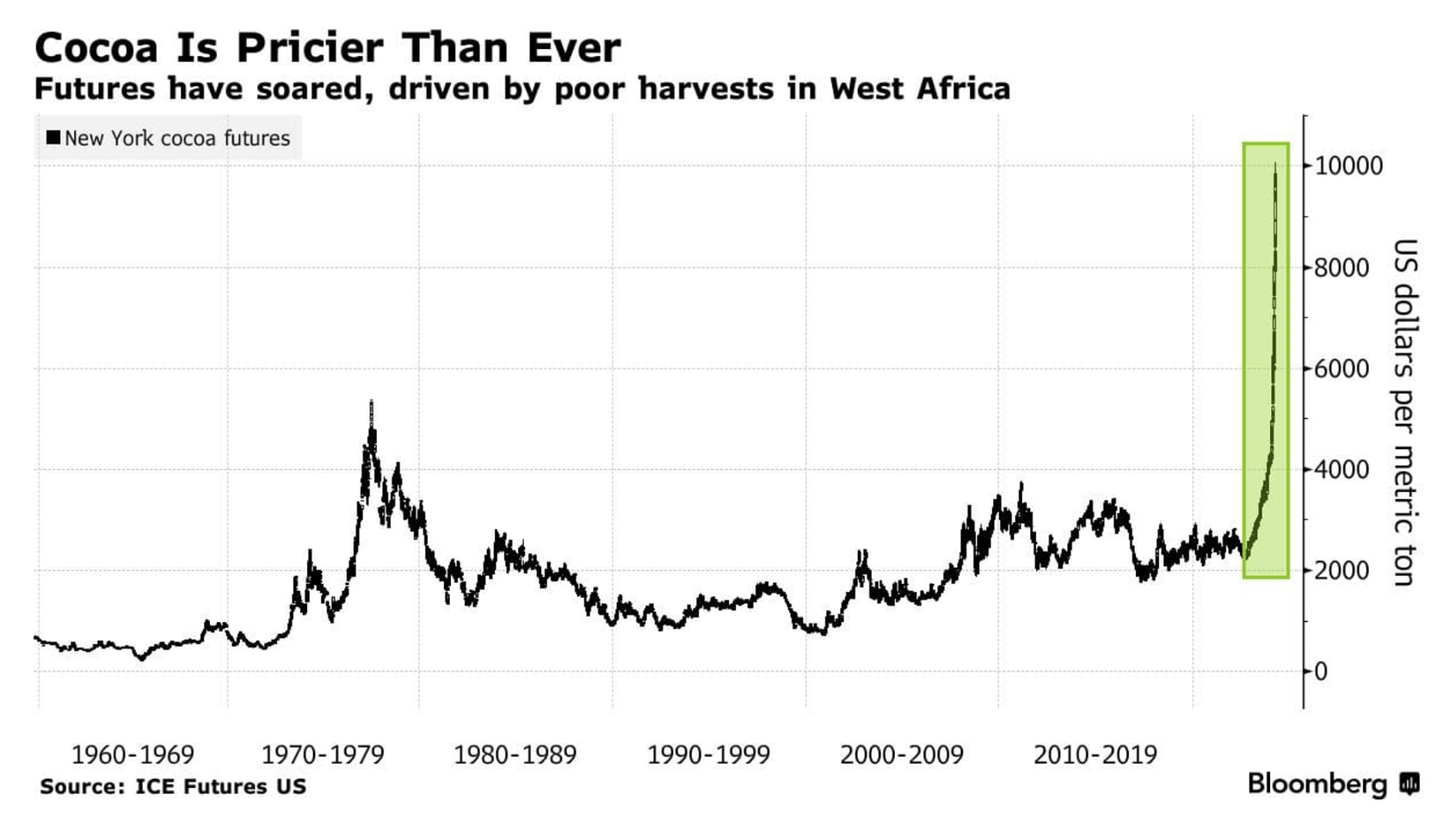

It’s now mid April, about a month after we wrote about cocoa bean prices skyrocketing from $2.3k per tonne to over $7k per tonne. And they are now at $10k per tonne … and it’s hard to see why they should stop there. Indeed I’m happy to wager a carton of any Cocoa Runners bars with anyone who will bet that cocoa prices will NOT go over $15k per tonne in the next 18 months – just email me (Note: to give any wagers a fair warning, in the 1970s; cocoa hit over $27k per tonne in inflation adjusted terms … at the same time, the “experts” differ – e.g., A team of JPMorgan Chase & Co. analysts forecast that cocoa prices will decline to around $6k.)

So we are going to do a deep dive over the next couple of weeks to try and answer a few key questions.

The first is WHY are prices skyrocketing .. and related to this, how likely are they to “stabilise” anytime soon? Is this about Global Warming, El Nino, the impact of wars on supply chains – and/ or is it something more structural?

The second is WHAT are the practical consequences for all those industries that rely on cocoa .. so not just chocolate and confectionery, but also cosmetics, ingredients companies and pharmaceuticals. How much will consumers see price rises ..

.. and WHO (if anyone), is likely to benefit (one would like to hope all can win, from farmers to consumers, via more craft chocolate), which countries and companies? And what are the potential ways for consumers to see some of the benefits here?

Why are cocoa prices skyrocketing?

“When the quantity of any commodity which is brought to market falls short of the effectual demand, … a competition will begin among them, and the market price will rise… When the quantity brought to market exceeds the effectual demand, it cannot be sold to those who are willing to pay… the market price will sink.” Adam Smith, Wealth of Nations, 1776.

The simplistic answer as to why cocoa prices are skyrocketing – as Adam Smith noted almost 250 years ago – is that there is a mismatch between the amount of cocoa being harvested and made available (ie supply), and global demand. Since Covid, demand for cocoa has continued to grow all over the world. At the same time, the amount of cocoa available has been squeezed. Stockpiles have been reduced, and a series of bad harvests, El Nino and other supply chain shocks (Ukraine, Gulf Wars) have challenged supply.

As ever, it’s also a little more nuanced and complex. For example Hedge fund traders have helped fuel these skyrocketing prices, investing literally billions of dollars via specially raised funds. Hedge funds saw not just rising demand and poor harvests, but they also were encouraged by the winding down of cocoa stockpiles – that had been used as a “buffer” by Big Chocolate to prevent West African Cocoa Trading Boards creating a successful Cocoa OPEC. Ironically short term traders are now pulling back as the market volatility is now too high – they literally can’t cover their positions.

The more interesting question is why, and how, did cocoa’s supply and demand become so unbalanced. And this is where the likes of “global warming”, deforestation, bad harvests and diseases are all cited as explanations. All of these factors are interlinked and all of these factors do play a role. But none of these factors are new .. so the question remains, why NOW?

WHY has this been allowed to happen? Only the most extreme climate change denier will dispute that climate change, particularly changing rainfall patterns and severe drought cycles when combined with ageing farmers and trees in West Africa has created an extremely exposed supply chain for Cocoa. We’ve also known about El Nino, and it’s potential impact, for a decade or more.. And as Dr Kristy Leissle notes “ the ICCO correctly predicted a few years ago, the various supply chain disruptions due to the pandemic, Panama canal closure, and wars have meant that critical farming inputs have not reached West Africa. With the poor weather already stressing trees, lack of farming inputs adds another layer of difficulty in keeping a farm healthy and maximally productive.”

The situation is tragically reminiscent of the parable of the frog in boiling water that doesn’t realise that what was initially tepid is slowly heating up and boiling it to death.

It’s also worth reinforcing that from a supply side perspective, the problem is primarily one in poor harvests of West African Commodity Cocoa, especially in the last 12-26 months that both buyers and suppliers warned about. Not all countries, cocoa qualities or even farmers in West Africa, have suffered from such downturns and extremes. So there looks to be something structural too.

Global Warming .. Water And Temperatures

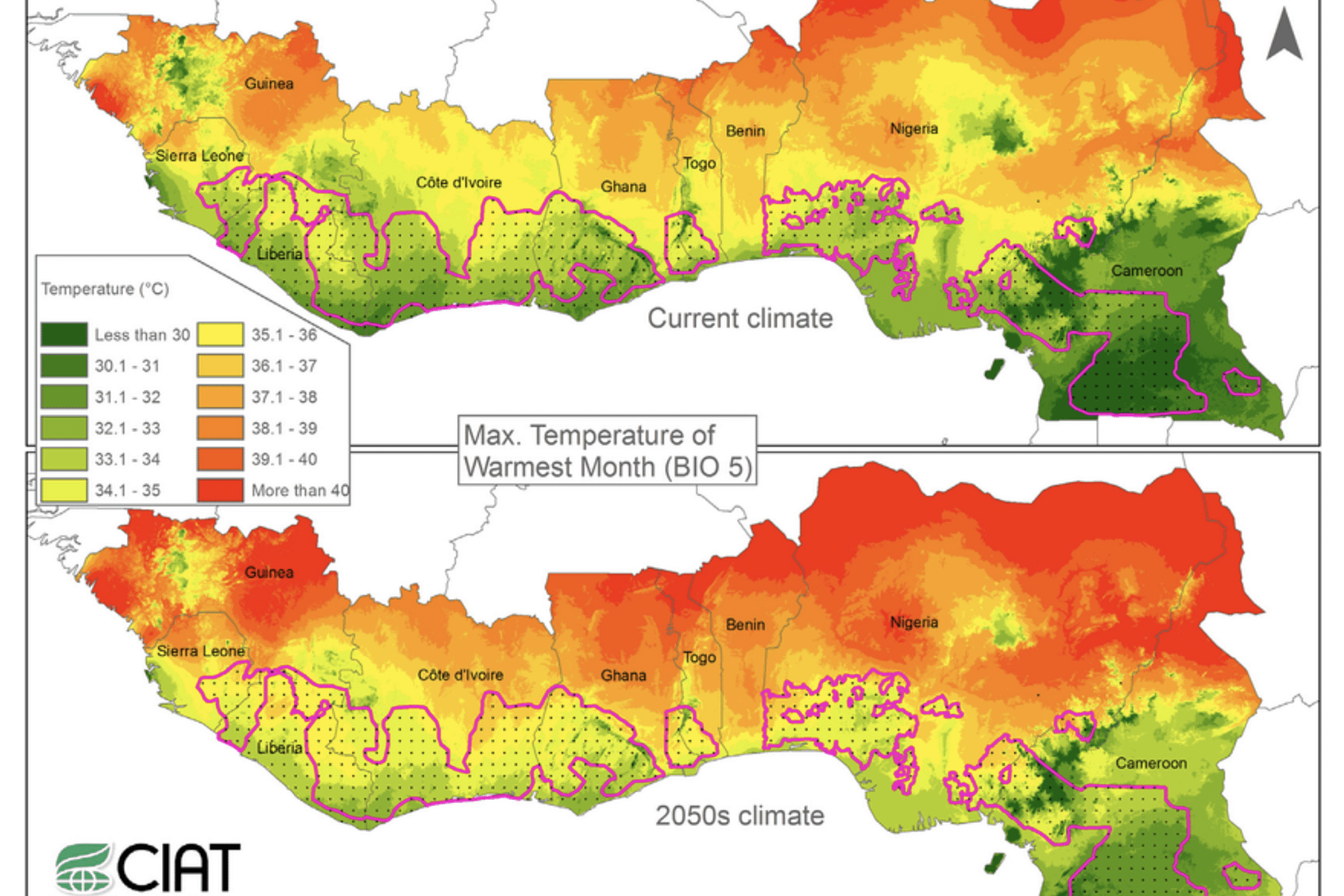

Global warming hasn’t suddenly materialised. The “Scylla” and “Charybdis” of drought/floods on the one hand and rising temperatures on the other hand have been around for decades. And serious as global warming is, most cocoa experts think we’re not yet at the point where cocoa can no longer be viably grown. Droughts (and floods) are increasing; but these can be handled via e.g., building of reservoirs, ponds, irrigation, etc. (and indeed this is being done in some places). Similarly we aren’t YET at the point where temperatures have risen such that cocoa cannot be grown in the “heartlands’” of West Africa.

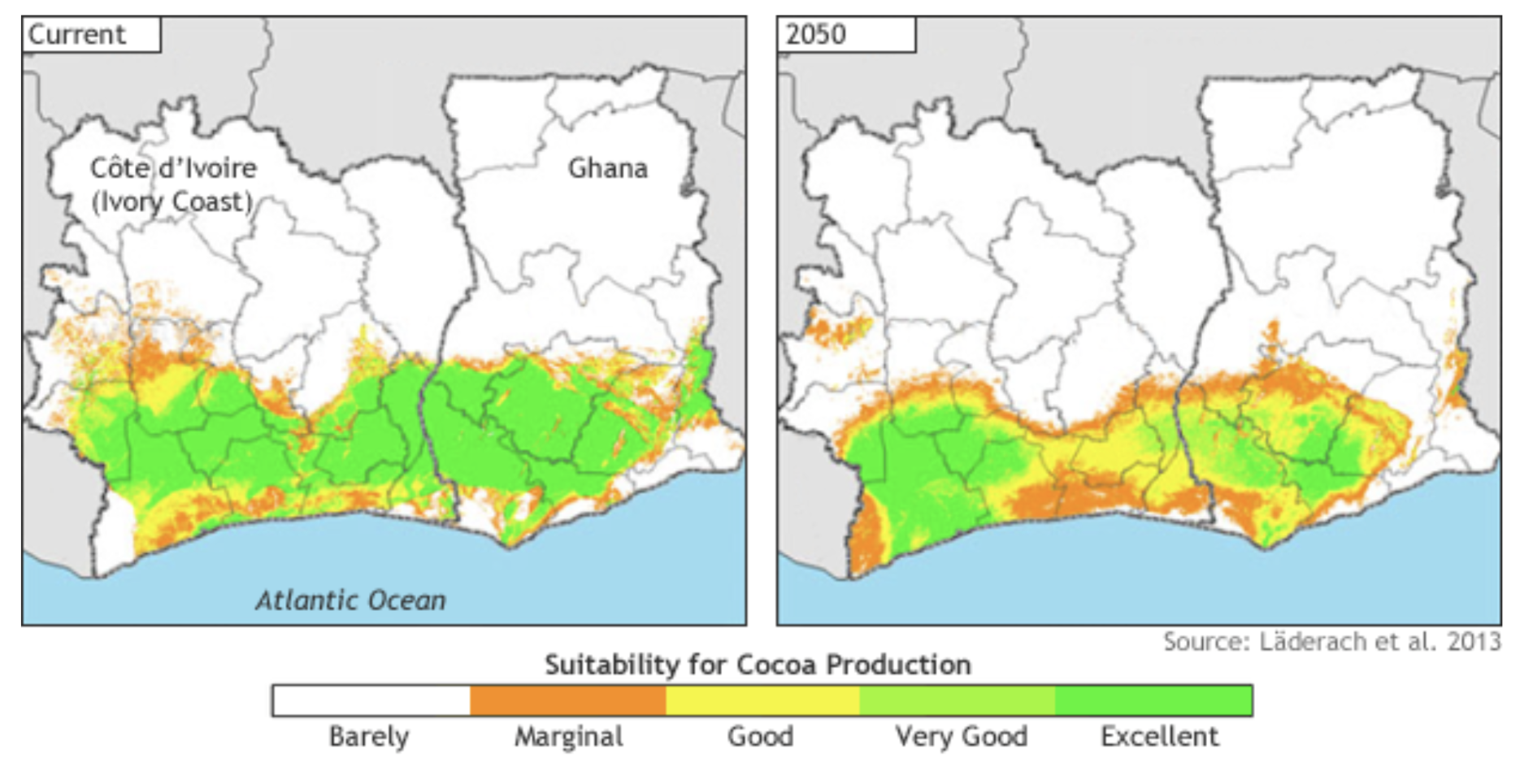

Note: this is NOT to deny the potentially devastating consequences of global warming for cocoa, especially in West Africa. Cocoa as a crop is extremely sensitive to changes in temperature; Theobroma Cacao only thrives within an ideal range of 15-30°C (60-86°F). So while we aren’t yet there, we are dangerously close .. and deforestation, by reducing shade, compounds this, and by 2050 the situation will be dire.

Deforestation

Deforestation also isn’t new .. It’s been occurring in most cocoa growing countries for decades. And again, whilst it’s a major problem it’s also sadly been a major contributor to some of the “growth” in cocoa supply. Much of the deforestation in West Africa in the 1990s and early 2000s came about from ongoing, year in, year out “death by a thousand cuts’ by small cocoa farmers trying to grow more cocoa and earn more cash. Today there is hardly any more rainforest to destroy.

So again, this definitely is a DISASTER . But it isn’t a sudden disaster.

Disease

Disease has historically been another massive factor for cocoa. If you want to explain the spread of cocoa around the world, from in the 16th century from Mexico to Ecuador, Brazil and Venezuela, and then in the 17th century to the Caribbean etc., disease is a key factor (See here). Plus in more recent times, the devastating disease known as witches broom did destroy the Brazilian Cocoa Industry in the 1990s (along with being arguably the first example of bioterrorism).

However, “swollen shoots virus” – the disease that is most often cited as “destroying” cocoa in West Africa – can be controlled. It’s been endemic in West Africa since the 1930s. And during this time cocoa scientists have found that “barrier cropping” (ie planting breakwalls of other plants like citrus or coffee) or even creating a 10m “cordon sanitaire” around cocoa farms can reduce swollen shoot virus by 85%. Effectively, the mealybugs that carry the disease, get “worn out” by these breaks. Scientists have also discovered that careful shade control, and removing alternative host trees (Cola chlamydanta, Ceiba pentandra, Adansonia digitata, Cola gigantean, etc) can stop the spread of the disease. But all of these approaches require education and investment, are most suited to medium to larger farms; they are very hard for small farms barely getting by.

Bad Harvests and El Nino

Without a doubt, recent harvests in West Africa have been – to put it mildly – “disappointing”. Harvests and yields have tumbled – often by over 60-75%. And there is no doubt that the floods, droughts, and extreme weather conditions of El Nino have been severe in Ghana and The Cote D’Ivoire.

But if it was “just” weather and El Nino, you’d have expected more uniformity across different farms and co-operatives, and even countries. And this doesn’t appear to be the case. Some farms and co-operatives have been able to grow; and yet next door farms and co-operatives have declined.

So if it’s not “just” disease, global warming, deforestation and El Nino etc. what else is happening here?

The Boiling Frog – A Case Of Unintended Consequences

Above and beyond global warming, deforestation, cocoa diseases etc. commodity cocoa – especially in West Africa (where over 70% of cocoa is now grown) – faces dire structural issues. For the last thirty years we in the West have enjoyed the delights of cheap cocoa. But this has been at the expense of the prices paid to farmers. And in turn, these low prices have created severity “structural problems” for West African Cacao. The average age of a cocoa farmer in the Cote D’Ivoire is now over 50. The average farm size of a cocoa farm is now farms are around 5.12 hectares in size, with an average of 3.61 hectares primarily dedicated to cocoa. This is way below the size that can justify a “cordon sanitaire” to head off swollen shoots virus, or dig a pond with irrigation pipes for water. The average daily pay of male cocoa worker is less than a $1, and female worker less than $0.50 – as opposed to the $2.50 that the World bank suggests as a minimum income to live in West Africa. So sending their kids to school can be a struggle, as can be affording pruning, purchasing vital fertilisers, etc.

Critics of capitalism and colonialism blame this on foreign multinationals abusing their dominant positions to drive down prices (and e.g., propping up kleptocratic and corrupt local elites, etc.) And it is extraordinary how “Big Chocolate” has for over forty years been able to stabilise,and even drive down, the inflation adjusted prices of cocoa, and how deforestation and underinvestment have run riot.

But whilst the “capitalistic” instincts of Big Chocolate are partly to blame here, the structural challenges in cocoa are also the result of unintended consequences and two countervailing forces in cocoa “selling” and “buying”. On the “buying” side, power has dramatically concentrated – and it’s the fiduciary duty of big chocolate to maximise shareholder returns by buying chocolate as cheaply as possible. On the supply side, the Cocoa Trading boards (COCOBOD in Ghana and the CCC in the Cote D’Ivoire) are mandated to protect the income of small farmers through collective bargaining and price setting. And with tragic irony, this has led to cocoa farmers being “squeezed” to grow more and more cocoa, at the lowest possible price, with minimal investment, replanting, training, etc.

Historically, the emergence of the Cocoa Trading Boards makes great sense – as does the logic behind “big chocolate” consolidating. Unfortunately, the combination of these two forces has created massive structural challenges for West African cocoa.

We’ve created a market structure of “Big Chocolate” buyers and National Cocoa Boards with misaligned long term incentives that, like the frog in boiling water, have slowly created a disastrous situation.

The History of the Cocoa Trading Boards

Back in 1937, cocoa farmers in Ghana went on a “sellers strike” and refused to sell their cocoa at the low prices demanded by European merchants for eight months. They successfully held out, and achieved higher prices for their beans. The British government then set up the Nowell Commission of Enquiry which in 1940 established the West African Produce Control board with a mandate to purchase cocoa under guaranteed prices for all West African countries. This was followed by the Ghana Marketing Board in 1947, with a similar mandate (but just for Ghana) and this eventually became COCOBOD. COCOBOD (and its predecessors) possess extraordinary powers. For example, one of its subsidiaries – CMC (Cocoa Marketing Company) is the ONLY authorised exporter of cocoa from Ghana. COCOBOD also sets a “floor” for cocoa prices, has a compulsory pensions program for cocoa farmers, provides credit, seedlings, etc. to farmers and much more.

In the Côte D’Ivoire, CAISTAB (Caisse de Stabilisation) was set up in 1955 with similar objectives (e.g,. it sets export prices, controls international cocoa sales, etc). And it too has an interesting history. Most famously in 1987, upset at falling cocoa prices, it organised a another “sellers strike”, banning exports of Ivorian cocoa beans for 27 months. At the same time, Président Félix Houphouët-Boigny of Côte d’Ivoire encouraged more cocoa growing; offering land and citizenship to new cocoa farmers promising that “la terre appartient à celui qui la cultive” (the land belongs to those that cultivate it). However President Félix Houphouët-Boigny failed to persuade other countries like Ghana, Nigeria, Indonesia etc. to join this “sales strike”. And such was the Côte d’Ivoire’s dependence on cocoa that they could not indefinitely maintain the strike. Eventually the Cote D’Ivoire returned to the market at lower prices, and were forced to submit to a donor-imposed program of economic liberalisation (but leaving in place CAISTAB, which later was renamed as the CCC).

So we’ve a situation in the two primary West African growers of cocoa where there are literally millions of farmers represented by very powerful Trade Marketing Companies.

Concentration of Supply Side (the buyers)

Back in the 1930s, and through to the 1960s, there were a relatively large number of foreign cocoa buyers of different sizes, all dealing with COCOBOD and CCC (and their predecessors). However in the last few decades there has been a huge consolidation such that a handful of big cocoa trading and processing companies (Callebaut, Cargill, Olam, etc.) and integrated chocolate and confectionery companies (Nestle, Mondelez, Hershey, Ferrero Roche, etc) dominate purchases.

These companies have a fiduciary duty to their shareholders to “maximise” returns. And this involves driving down the prices of commodity cocoa. To a cynic, the current system of dealing with Cocoa Trading Boards gives Big Chocolate a classic cover to deflect charges that they are responsible for the low incomes of cocoa farmers in West Africa, the lack of training, challenges of disease prevention, lack of programmes to plant new trees, etc..

The big confectionery makers and big cocoa trading companies know full well that e.g, over 85% of the cocoa farmers in West Africa are living below the suggested minimum income – every year they commission reports that clearly state these facts, and they’ll market some great new “approach” to educate the children of farmers, provide free school meals, etc. The same is true on deforestation, average age of cocoa farmers, etc. They too are topics with LOADS of reports and initiatives.

Big Chocolate operates at “arms length” – and indeed in many cases doesn’t even know where the cocoa they are buying comes from (See above and below). And so how can they be held responsible for cocoa farmers not receiving Western style “fair wages” if they don’t directly set prices etc? Big Chocolate has spent literally millions of dollars on initiatives like the World Cocoa Foundation, and on multiple other projects in deforestation (admittedly these “millions of dollars” are a fraction of the dollars it spends buying cocoa). But the current setup, where the majority of cocoa purchased in e.g., the Cote D’Ivoire, isn’t traceable makes it logistically far, far harder to – for example – work with farmers to plant more trees, educate farmers on how to deal with pathogens and diseases, etc. This isn’t like one of their factories or processing plants which they directly manage and so are directly accountable for health and safety, training, paying minimum wages, etc.

This slow evolution of an industry where cocoa has been “commoditized” and there are fewer and fewer buyers, smaller and smaller farm plots, older and older trees etc. has created a perfect storm that neither the Big Chocolate as Buyers nor Cocoa Trade Marketing boards as Sellers, can easily address. To offer a simplified caricature, for the last few decades up until the recent skyrocketing of process, the way that the structure of “buyers” and “sellers” in Western cocoa has (accidentally) evolved has meant that consumers have been able to enjoy cheap chocolate treats at the expense of West African cocoa farmers and their families (and, see above the rainforest, planet etc.). But we are now all – literally – paying the price, and it’s hard to see how cocoa prices will fall back down any time soon.

Changing this isn’t going to be easy. Cocoa is CRITICAL to the economies of both Ghana and the Cote D’Ivoire, accounting for over 30% of Ghana’s export earnings and employing over 17% of Ghana’s workforce – and for the Cote D’Ivoire the figures are even higher, accounting for 58% of exports and over 20% of its workforce’s livelihood. The political classes and trading companies are intimately linked together.

And even if somehow the political and infrastructural will somehow materialise in both Big Chocolate and the governments of Ghana and the Cote D’Ivoire, it takes 3-5 years for new cocoa trees to bear fruit. Training farmers to prune their trees, avoid diseases, etc. takes less time – but it still requires a lot of people, education and will.

MAYBE the harvests in 2024 and 2025 will be far better than expected, despite El Nino, etc.. But fixing these structural issues is going to take a while. Blaming global warming, diseases, bad harvests and even El Nino misses the fundamental problem that we can’t continue to expect cheap cocoa prices at the expense of cocoa farmers who can’t afford to plant new trees, dig ponds, invest in shade coverage, etc.

A case study -the plight of one cocoa farmer (courtesy of Dr. Kristy Leissle, Founder & CEO ACM)

To put all of this into perspective, African Cocoa Marketplace (ACM) has just produced a dramatic video and case study of John Narh Adamnor, a small-holder cocoa farmer in the Eastern Region of Ghana. He has a 3-acre plot that has been in his family for over 60 years, and his trees used to produce approximately 15 bags of cocoa each year, ‘But this year, I couldn’t get even 5 bags. ‘This shows that cocoa has failed us,’ he says.

The good news is that COCOBOD in Ghana has increased its prices by 58.26%, from GH¢20,928 per tonne to GH¢33,120.00 per tonne, following a similar move by neighbouring Cote d’Ivoire, which hiked its cocoa farmgate price by 50% from 1000 FCA francs to 1500 CFA francs. But even though the producer price has risen by close to 60%, John’s yields have fallen by two-thirds. So even at the new, higher producer price, his total earnings for the main crop would have been just $770. As Kristy writes “For John, any benefit from the producer price rise is more than cancelled out by his dramatically lower yield”.

John blames much of this on climate change, in particular with changes in the timings or rain. He says the trees themselves are healthy but need the required amount of rain to fruit. So he is praying for rain to mature his mid-crop, which starts soon in May. As he notes in a a video produced by the (African Cocoa Marketplace, “the region would normally have expected plenty of rainfall by April), but when the rains don’t come, work like pruning is delayed … (and) if the sun persists, the trees can die.

Some grounds for (cautious) optimism .. but there are no “silver bullets”

At the same time, there are some encouraging signs. There are some amazing cooperatives like Abocfa or Kuapa Kokoa in Ghana. And we’re hugely excited by Lesley Agyare’s Three Mountains Beans that a bunch of makers are experimenting with, and we hope soon to be able to retail.

But more fundamental changes are required. And hopefully the rise in cocoa prices will enable some of these to start. For example, in other parts of the world (e.g, Colombia and Brazil), larger farms have been investing in ponds and irrigation pipes to deal with the dramatic fluctuations in rainfall). And they’ve built “cordon sanitaire” as a bulwark against disease, etc.

Addressing these structural challenges is, and will continue to be incredibly important and difficult. To be fair to Big Chocolate and to the Cocoa Trade Boards, it’s in their interests to address these issues .. but the current incentives and structures make this very hard.

And there are no “silver bullets”. For example, “Fair Trade” is AWESOME for many crops, but it’s not ideal for Cocoa and although the likes of Abocfa have massively benehectied., Fair Trade has achieved only limited “cut through”– see here for more.

Similarly Tony’s marketing is impressive. But please remember that by their own admission over 10% of the farms they source from employ child labour, the primary ingredient in 8 of their 9 bars is sugar (and sugar has as horrific a problem of workers rights as cocoa and no, Tony, won’t say where their sugar comes from) and it’s not easy to work out what the “Tony Premium” really amounts to for farmers) – see here.

It’s not easy to see a simple solution – there really are no silver bullets. But at the same time, it’s clear that there is a structural problem with West African Cocoa that is exacerbating the problems of Climate Change, Deforestation, El Nino, the impact of war on supply chains, etc. The current situation of a concentrated number of Big Chocolate Buyers versus National Cocoa Boards in West Africa is compounding these problems. We have to move on from seeing cocoa as “just” a commodity, with Big Chocolate fixated on low costs and high volumes where they are operating at arm’s length, and with very different objectives, to the West African Cocoa Boards.

Cocoa has more complexity of flavour than just about any other food (or drink). Plus thanks to cocoa butter, chocolate has a mouth feel that not just delights texturally, but also releases these aromas. And as Craft Chocolate shows, if you pay farmers fairly with long term commitments, they can grow great beans from which you can craft amazing chocolate bars. You can pay farmers to invest in the future of cocoa, rather than negotiating on yearly price levels and volumes. This is a very different paradigm and requires major shifts in how we consumers think about chocolate .. and how the industry itself is set up. But we think it’s worth it.

Next week we’ll continue this more optimistic tack, exploring some of the potential “silver linings” from these price rises (as well as some of the challenges; hint: if you are a fan of white craft chocolate bars, enjoy them while you can!)

Thanks as ever for your support

Spencer

Sources:

https://www.intechopen.com/chapters/68225

https://link.springer.com/article/10.1007/s13593-018-0538-y

https://journalofeconomicstructures.springeropen.com/articles/10.1186/s40008-019-0135-5

https://cocoadiaries.substack.com/p/part-1-are-we-all-complicit-the-complexities

https://voicenetwork.cc/cocoa-barometer/

www.Ajol-file-journals_250_articles_234355_submission_proof