Cocoa prices 2026 update

For most of the last thirty or more years the price of commodity cocoa has been ground down, and – in real terms – at best flat. Then for much of 2024 and 2025, cocoa prices skyrocketed. They gave AI and crypto stocks a run for their money. Cocoa futures surged to unprecedented levels, driven by poor harvests in West Africa, diseases and pests, ageing tree stock, climate volatility, and long-term underinvestment at farm level. Dramatically increased chocolate prices followed. Panic narratives took hold. The popular press had a field day over shrinkflation and the end of chocolate as we’d known it.

In early 2026, the prices of commodity traded cocoa have come sharply down from these peaks. Big Chocolate has managed to reassert some control, and found a way to manage prices (and hence what it pays to cocoa farmers) down. However the structural problems remain and this isn’t a simple “return to normal”.

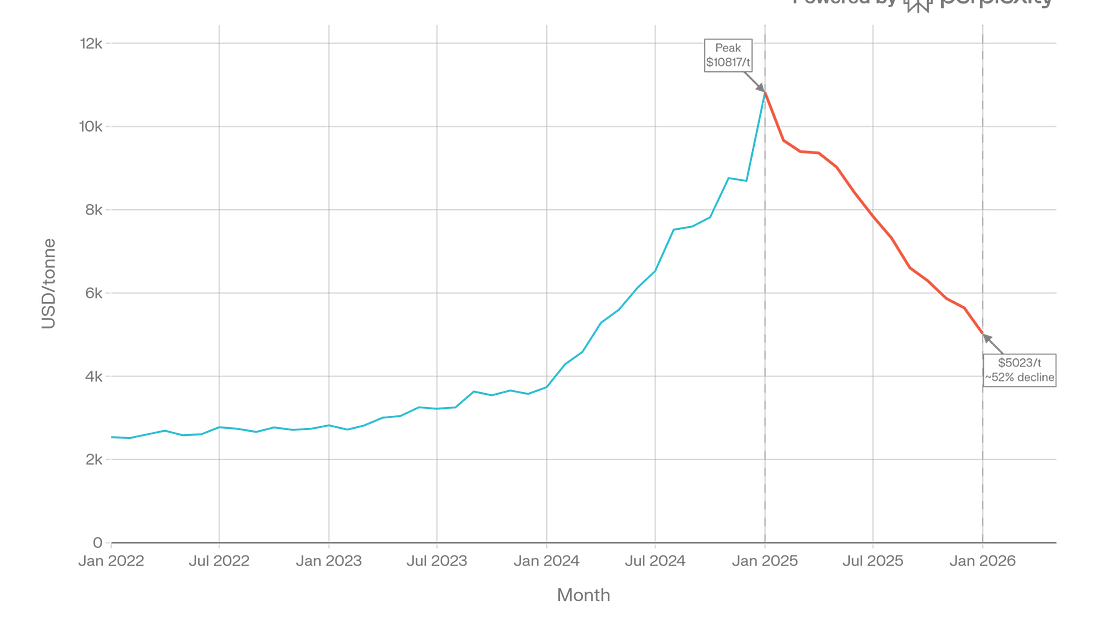

Futures Have Fallen – But They’re Still High

Cocoa futures on ICE London and New York have retreated materially from the extremes of 2024–25. On a quarterly average basis, prices have fallen by roughly half from their peak.

That sounds dramatic – but even after this pullback, cocoa remains structurally expensive by historical standards, trading well above the levels that defined the market for most of the last 20 years.

This matters because the commodity chocolate industry built its economics, and products, for cocoa to be priced at USD 2,300–2,800 per tonne. That world has not – yet? – returned.

Demand was constrained – it’s not about Supply Recovering

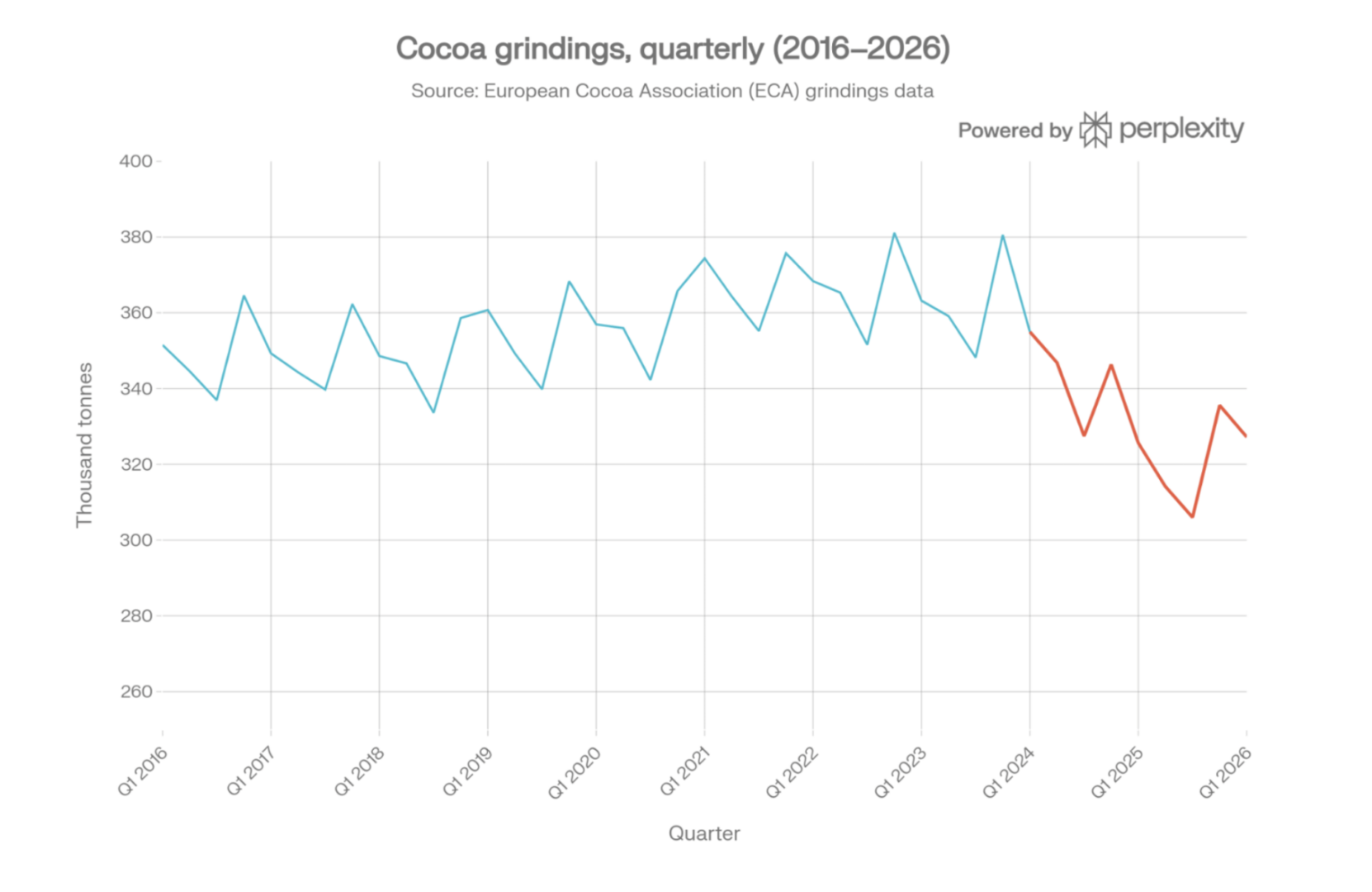

The most important shift in the last 6–12 months hasn’t been on farms. It’s been in factories.

As cocoa prices surged, manufacturers slowed down, reducing the size of bars and replacing cocoa for other “additives” (sugar, other fats, etc.). The clearest way to see this is looking at grinding data from Europe and Asia which show a persistent decline in cocoa processing volumes, even as prices were still elevated.

European cocoa grindings index

To put it another way: rather than paying more for cocoa, and rather than seeing cocoa demand continue to exceed anticipated harvests, the big cocoa processors and chocolates makers have been using less cocoa. This reduction in grindings has enabled Big Chocolate a way to push prices down not because cocoa suddenly became abundant, but because buyers bought less.

“Surplus” Doesn’t Mean Safe

Analysts are now forecasting global cocoa surpluses for upcoming seasons, following several years of deficit. On paper, that looks reassuring and there are some reassuring signs.

In reality, it’s fragile. West Africa still dominates global supply, and the same structural problems remain unresolved: ageing trees, changes in rain flow, disease, low farmer incomes, and high exposure to weather shocks. A single poor harvest or logistical disruption could/will tighten the market again very quickly. And over the longer term unless more young people become cocoa farmers, unless more cocoa trees are planted, more investment is made in irrigation facilities and wells, etc. the writing is on the wall.

The current price environment reflects temporary balance forced by a decline in grinding volumes. It’s not a stable, long term solution.

Why higher prices aren’t really benefiting most farmers

One of the biggest misconceptions in cocoa economics is the belief that higher commodity futures prices automatically translate into higher real incomes for farmers. In reality, the system isn’t that simple firstly because of the way the market is structured (and can be gained) and secondly because of declining cocoa yields.

The global reference point for cocoa is the London cocoa futures contract traded on the Intercontinental Exchange (ICE). This market is where traders, processors, buyers, and investment funds hedge and speculate daily on expected supply and demand. Prices can move violently on sentiment, forecasts, weather models, and financial positioning. And it’s spikes on this market that have caused supermarket chocolate bars to simultaneously shrink, become more expensive and contain less chocolate.

What they haven’t done is lead to higher prices for farmers.

West Africa – which produces roughly two-thirds of the world’s cocoa – operates under a fundamentally different pricing model to cocoa futures. Prices are set centrally and fixed administratively, season by season. In Ghana, the Ghana Cocoa Board (COCOBOD) announces a guaranteed producer price at the start of the season. In Côte d’Ivoire, the Conseil du Café-Cacao (CCC) sets minimum farmgate prices and controls sales structures. These systems are designed to stabilise farmer incomes ahead of harvest and provide some certainty. Farmgate prices are deliberately kept “sticky” to provide predictability for millions of smallholders. There is a structural disconnect between headline cocoa prices and what farmers actually earn.

When futures prices briefly surged above US$10,000 per tonne in 2024–25, many assumed that – finally – farmers would be paid more. In practice, the gains reaching farmers were muted. Farmgate prices had already been fixed months earlier and did not rise in step with the spike. When global prices later fell back sharply, the imbalance flipped: farmers were left exposed to the downside without ever having captured the full upside.

By late 2025, Ghana had set its official farmgate price at around GH¢58,000 per tonne (roughly US$4,640/MT), while Côte d’Ivoire fixed its minimum at about 2,800 CFA francs per kilo (around US$4,900/MT). These were historically high nominal prices. Yet as international markets retreated from their peaks, those fixed minimums at times exceeded futures-derived equivalents.

Yields

Crucially, price is only half the income equation. The other half – often ignored – is yield. And yields across West Africa have been falling for years. That is to say, the amount grown per hectare has been falling.

In Ghana, many smallholders now harvest just 300–400 kilograms per hectare, far below the agronomic potential of 800–1,000 kg/ha, and well below what is required for a viable livelihood. Cocoa trees are aging – most are 25 to 40 years old – while swollen shoot virus, black pod disease, fertilizer shortages, and increasingly erratic rainfall steadily reduce output per farm. Côte d’Ivoire faces the same dynamic. For decades, national production growth came primarily from destroying the rainforest to expand cultivated area rather than improving productivity. That land-led model is now largely exhausted, leaving declining yields exposed (see here).

As Kristy Leissle has clearly articulated in some great videos a higher price per tonne does little good if farmers are producing fewer tonnes. A Ghanaian farmer earning around US$4,600 per tonne but harvesting half the volume they did a decade ago is worse off in real terms – especially once rising input costs, labour shortages, and inflation are taken into account.

So even with higher global prices and elevated official farmgate rates, falling yields mean take-home incomes remain fragile. In Ghana, that gap is already pushing some farmers toward illegal gold mining, which offers faster cash returns, or toward cross-border leakage, selling cocoa into neighbouring countries such as Togo where payment timing or terms may appear marginally more attractive.

One important other clarification: In Ghana and Côte d’Ivoire, where prices are centrally set by COCOBOD and the CCC respectively, claims by major chocolate companies (including those with four letters starting with T and ending in Y) that they’re “paying farmers more” require context. It sounds great to say they want to pay farmers more in “their” supply chains. But the reality is that they can’t. Even amazing marketing slogans claims can’t override national pricing systems, and most cocoa farmers still aren’t taking home anywhere near a “minimum living income”.

So what’s the REAL problem?

Over the past fifty years, cocoa in West Africa has been reshaped by two forces above all others: firstly commoditisation and consolidation by the buyers and secondly deforestation and threadbare incomes for farmers.

Commodity cocoa has been stripped of origin, flavour, and direct stories. It’s been reduced to a generic industrial “commodity” input. At the same time, purchasing and processing power collapsed into very few hands. Today, just three companies — Barry Callebaut, Cargill, and Olam — control roughly 60–70% of global cocoa grinding capacity, and purchase the vast majority of cocoa grown in West Africa.. Their business model depends on scale, uniformity, and buying cheaply. They’ve even successfully lobbied for chocolate to be exempt from country of origin rules (ie maker don’t need to say where they source their chocolate on bars) on the grounds that this would confuse consumers and raise prices unless they could “switch” between makers (See here – and also note their argument that they should be exempted from country or origin rules for chocolate because the primary ingredient in most of their chocolate bars and snacks is sugar).

Over the last thirty plus years, this oligopoly and concentration of purchasing, in combination with commodisation of cocoa into a fungible ingredient has enabled these Big Chocolate companies to hold, and drive down, prices.

Small holder farmers with cocoa as their only cash crop don’t have many alternatives other than to try and grow more with less “inputs”. So they’ve cut down more and more of the rainforest to grow more. Côte d’Ivoire and Ghana alone have lost over 80–90% of their original forest cover since cocoa expansion began (see here on EUDR for more). According to the International Labour Organization, around 1.5–1.6 million children are still involved in hazardous labour in cocoa-growing regions (see here for more on child labour).

It’s not part of some dastardly malicious plan. But it is the inevitable outcome of a system designed to deliver vast volumes of cheap, interchangeable cocoa.

Cheap chocolate wasn’t free — someone else paid

There is a “positive” side to this history, at least for consumers in wealthy countries. For decades, it has delivered astonishingly cheap chocolate: £1 bars, buttons, snacks, and novelty confectionery available everywhere, all the time.

But that cheapness came at a cost that was simply pushed out of sight — onto farmers, landscapes, and, eventually, public health.

Chocolate was arguably the original junk food. Long before crisps and fizzy drinks, it pioneered the industrial playbook: the “bliss point” of sugar and fat, hydraulic presses, emulsifiers like soy lecithin, and ultra-portable formats designed for constant snacking. As the historian Sidney Mintz put it in Sweetness and Power, sugar — and by extension sweetened chocolate — became “a daily necessity rather than a luxury, embedded in the rhythms of industrial life.”

Today, ultra-processed foods account for around 55–60% of calories in the UK and US. The health consequences are no longer abstract: rising obesity, metabolic disease, cardiovascular illness, and diet-related cancers. Cheap chocolate didn’t just mirror that trend — it helped invent it (see here for more and our take on GLP1s).

There is an alternative — it’s worked elsewhere

The alternative isn’t to abandon chocolate altogether or pretend snacks don’t exist. It’s to rethink what we eat and how we eat it.

Other industries have already shown what that transition looks like. Specialty coffee now accounts for over 20% of coffee sold in many developed markets. That shift didn’t only benefit a niche of farmers and roasters. It lifted expectations across the whole category — better flavour, clearer origin, higher prices justified by quality, and more money flowing upstream.

The same pattern is visible in bread, cheese, beer, and wine. When consumers learn to value flavour, craft, and provenance, markets reorganise. They’ll pay a bit more for quality and think about prices, farmers, the environment and their health.

Craft chocolate is pursuing a similar transformation, yet it still accounts for well under 0.5% of the global market. Several factors explain this lag. Unlike speciality coffee or craft beer, craft chocolate isn’t a simple “upgrade” .So for example, it’s far easier to upgrade when the “hit” from caffeine (or alcohol) is the same in specialty coffee as it is in mass market coffee, and craft beer or mass market beer, the “addictive” element in mass produced chocolate – SUGAR – isn’t in chocolate. Similarly, coffee and beer are far more “social”, and hence it has been easier for specialty coffee and craft beer to go “viral”. Mass market confectionery is all too often a guilty, private treat / pick me up from a vending machine consumed in a rush. However once people discover the delights of sharing and savouring craft chocolate, they “get” it … come to a tasting to explore more and spread the word.

A Radical Alternative

There is an even more radical alternative development. As the impact of reducing grinding volumes on spot cocoa prices demonstrates, even after a string of bad harvests, it doesn’t take too much for Big Chocolate to find a demand side solution to the problem of falling supplies. Smaller bars. Higher prices. And cocoa substitutes.

A lot of chocolate isn’t consumed just as chocolate. Chocolate is also consumed in cakes, ice creams, drinks, snacks etc. And it’s far, far easier to use “cocoa alternatives” in these products. Indeed lots of classic chocolate snacks are being rebranded as “chocolate flavoured”. To date much of these “alternative cocoas” have been replacements for cocoa butter (the so called cocoa butter alternatives – aka vegetable fats, synthetic alternatives, palm oils etc.). This is because cocoa butter has been incredibly expensive, and even though it’s mouthfeel is unique, it can up to a point be replaced with other fats. Replacing cocoa mass has been less explored, partly because it’s historically been cheaper and partly because it’s been really hard to replicate the wonderfully complex flavours of chocolate.

But there are now a bunch of startups actively exploring this space – and Big Chocolate is actively investigating.

And if European, American and Asian grinders start to use the synthetic cocoa alternatives, they’ll be able to keep up the demand squeeze even if supply remains constrained.

What This Means for Craft Chocolate

Large industrial chocolate companies hedge, reformulate, and smooth volatility through scale. And they may even be able to drive prices back down via alternative, synthetic chocolate and/or shrinkflation, etc.

Craft chocolate makers cannot and won’t go down the route of alternative, synthetic cocoa. They buy the finest beans, agree long term contracts that are transparent (see here for transparency reports from Taza, Askinosie, Marou and Uncommon). Craft chocolate makers pay premiums for quality, traceability, and fermentation. And they feel price rises with a delay, because contracts and inventories lock in yesterday’s costs.

Where We Are Now

Cocoa prices are no longer rivalling AI stocks. Prices are lower than the panic highs of 2024–25, yet still far above long-term norms. Demand has softened as the big chocolate houses are grinding far less. That’s been enough – for now – to match supply and demand so that prices can be pushed back down. And they may be able to continue this imbalance if they actively pursue synthetic cocoa.

For craft chocolate, this moment is painful. We’ve always been willing to pay higher prices and sign long term contracts that reward and incentivise farmers over the long term. And we need to keep reminding consumers that chocolate made slowly, transparently, and with flavour at its heart is still great value – and not about being “cheap” or “great deals” etc.

So sorry. Craft Chocolate prices over the short to medium term aren’t going to fall. But we think that Craft Chocolate is still amazing value.

Sources

Cocoa prices, futures, and grindings

Barchart – “Where Are Cocoa Prices Heading?” (2025) https://www.barchart.com/story/news/32493753/where-are-cocoa-prices-heading

Trading Economics – “Cocoa – Price – Chart – Historical Data – News” https://tradingeconomics.com/commodity/cocoa

ICE – “Cocoa Futures” https://www.ice.com/products/7/Cocoa-Futures

Barchart – Cocoa Dec ’24 Futures Price

https://www.barchart.com/futures/quotes/CCZ24

Bloomberg – “Cocoa Hits Two-Year Low as Europe Grinds Fewest Beans Since 2013” (2026) https://www.bloomberg.com/news/articles/2026-01-15/europe-cocoa-grindings-sink-more-than-expected-as-demand-craters

Ecofin Agency – “Cocoa Grindings Fall Globally as High Prices Weigh on Demand” (2025) https://www.ecofinagency.com/news/1807-47761-cocoa-grindings-fall-globally-as-high-prices-weigh-on-demand

CocoaIntel – “Europe and Germany Cocoa Grindings Decline in Q4 2025” (2026)

https://www.cocoaintel.com/germany-and-europe-cocoa-grindings-decline-in-q4-2025/

Farmgate prices and West African pricing systems

COCOBOD – “Review of producer price for the 2025/26 cocoa season”

https://cocobod.gh/news/review-of-producer-price-for-the-202526-cocoa-season

COCOBOD – “Government announces producer price of cocoa for the 2025/2026 cocoa season” https://cocobod.gh/news/government-announces-producer-price-of-cocoa-for-the-20252026-cocoa-season

Ghana Agricultural Chamber – “COCOBOD maintains cocoa producer price despite Côte d’Ivoire hike” https://ghanaagricchamber.com/4/16/74/cocobod-maintains-cocoa-producer-price-despite-c%C3%B4te-d%E2%80%99ivoire-hike

Mordor Intelligence – “Chocolate Market Size, Trends, Share, 2031 Report”

https://www.mordorintelligence.com/industry-reports/chocolate-market

Ultra-processed foods, diet share, and health

Newsweek – “The Ultra-Processed Foods Adding Most Calories to US Diet” (2025) https://www.newsweek.com/ultra-processed-foods-adding-most-calories-us-diet-2110104

University of Cambridge – “Ultra-processed food makes up almost two-thirds of calorie intake of UK adolescents” (news release) https://www.cam.ac.uk/research/news/ultra-processed-food-makes-up-almost-two-thirds-of-calorie-intake-of-uk-adolescents

MRC Epidemiology Unit, University of Cambridge – Blog on ultra-processed food and UK adolescents https://www.mrc-epid.cam.ac.uk/blog/2024/07/17/upf-two-thirds-calorie-intake-uk-adolescents/