The rising price of cocoa

Over the last few months the spot price of commodity cocoa has skyrocketed, literally more than doubling to nearly $7,000 per tonne; exceeding the all-time high cocoa prices last seen in the 1970s. And there is no sign of commodity prices cooling down. The Financial Times has reported that two hedge funds have committed over $8.7BN to “investing” in this play. And even though prices have doubled, for commodity cocoa prices to regain the levels of the 1970s in real (i.e. inflation adjusted) prices, they would need to be at over $25,000 – so another 3-4 times.

This isn’t good news for mass market, ultra processed confectionery – especially as much of this skyrocketing has been AFTER most high street brands dramatically increased retail prices post Covid.

It’s going to be complex and very messy. A few big hedge funds will make a fortune. A few smaller “pisteurs” and “traitants” (the cocoa intermediaries in West Africa sitting between “big chocolate” and cocoa farmers) may enjoy a bonanza. Consumers are going to face higher prices for mass market confectionery (the price of the main ingredient in most chocolate snacks, sugar, has also been shooting up). There will be more use of what’s known as “CBRs” (cocoa butter replacements, aka palm oil, hydrogenated vegetable fats, etc.).

West African Cocoa farmers are unlikely to see much of the upside. To date, even though the cocoa price has doubled in New York, this has only led to a 10% rise in prices paid to farmers in Cote D’Ivoire (the world’s largest grower of cocoa). And it’s unfortunately hard to see how these price rises are going to address the chronic and systemic problems of underinvestment in cocoa farming, end deforestation, pay farmers so that the crimes of child slave labour are ended, stop the spread of “swollen shoot” and other cocoa diseases, etc.

It’s not clear that there is a “silver lining” for Craft Chocolate either. Craft Chocolate has always paid higher prices to its farmers (traditionally paying 3-10x higher prices than commodity cocoa) for high quality, flavoursome beans. The price of these craft chocolate beans will also rise. And HOPEFULLY consumers will continue to realise that the only way to address the systemic problems of Big Chocolate and commodity cocoa, is by focusing on quality and flavour, paying farmers fairly, with long term commitments, encouraging them to invest in cocoa’s future. So please upgrade! There has never been a time more critical to swap from scoffing lots of cheap confectionery made with commodity cacao.

To try and understand what’s behind the spectacular spike in cocoa prices and its implications, we’ve assembled a bunch of charts and analysis that try to explain:

- The overall structure of cocoa, and how “big chocolate” has – until recently – been able to commoditise cocoa without much investment in farms, farmers, etc.

- The specific conditions that have led to the dramatic spike in prices

- What’s like to happen next (yes, prices will continue to go up, there will be shrinkflation, etc)

- How this MIGHT give some grounds for hope if we in Craft Chocolate can reinforce our focus on quality and flavour.

HOW DID WE GET HERE – THE STRUCTURE OF COMMODITY COCOA TODAY

There are a number of great books on Cocoa starting with Dr Kristy Leissle’s “Cocoa” (see here), but here is a quick 101 overview:

- Even though Theobroma Cacao (the tree that cocoa pods grow on) originated in South America (see here), most of the world’s cocoa (over 75%) comes from West Africa. The Ivory Coast is the largest “powerhouse” (controlling 40%) followed by Ghana, Cameroon, and Nigeria who account for another 35% to 40% of total cocoa grown.

- Supply and Demand are very unbalanced in terms of concentration; there are lots of suppliers and few buyers.

a) Most West African cocoa is grown by 5m+ smallholder farmers who have farms of less than 4 hectares, and grow on average 600-800 KGs per year (so say enough cocoa to make around 1,500 – 2,500 bars high percentage chocolate)

b) Most of this cocoa is purchased by a handful of cocoa traders and processors who few of us will have heard of (e.g., Olam, Callebaut, Cargill, Ecom, Sucden) and they purchase directly, and indirectly, without “owning” farms. - To try and level the playing field, and counteract this oligopoly, the governments of Cote D’Ivoire, Ghana, etc. have cocoa trading bodies who try to set a floor for cocoa prices, and also try “buy forward” farmer’s cocoa crops (note: these boards have a long history, dating back to the 1930s and earlier, to deal with the problem or rapacious imperial multinationals)

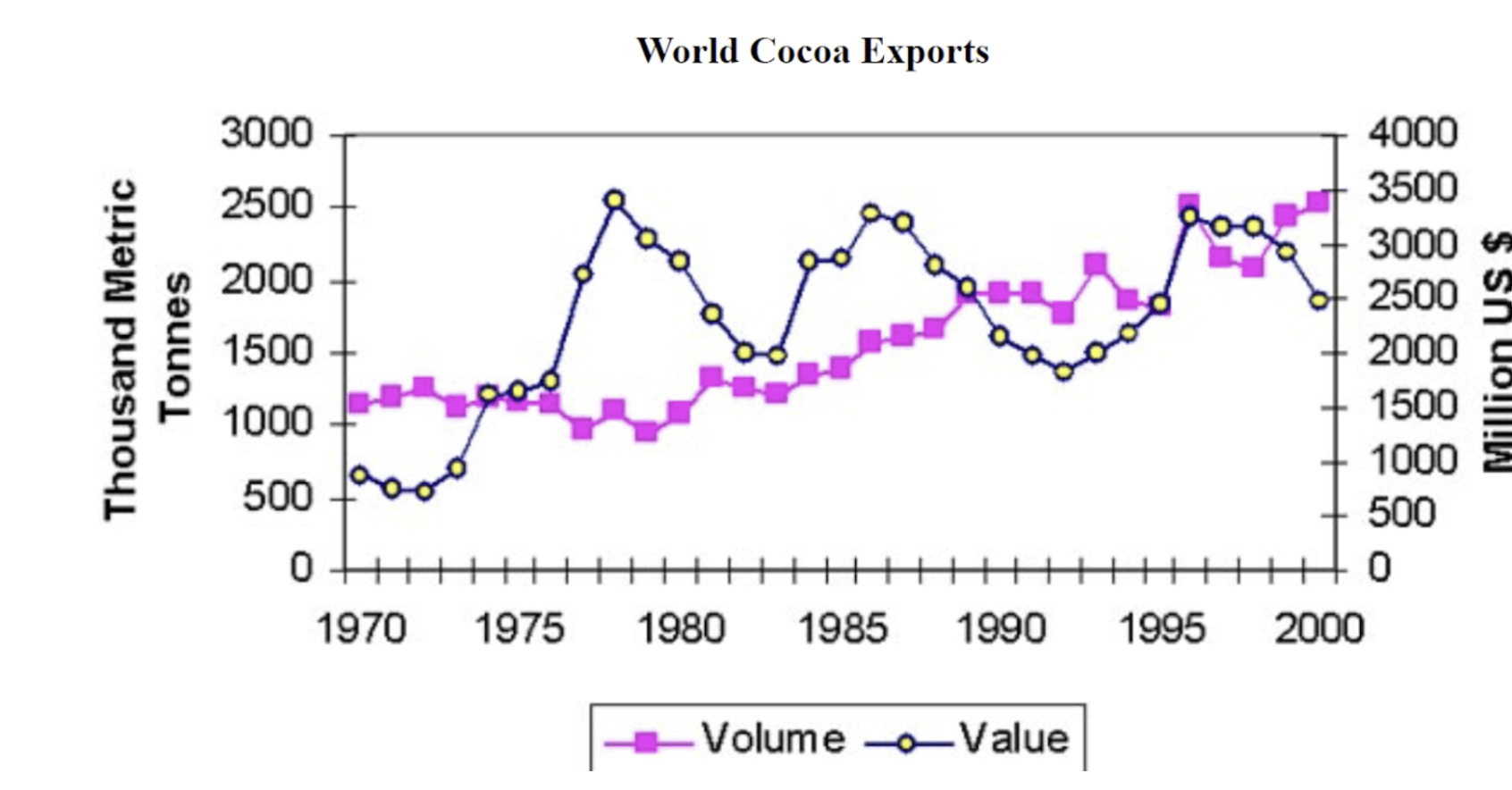

- Demand for cocoa has been growing dramatically over the last few decades

- However “Big Chocolate” has managed to keep the price of cocoa “steady” – so even though more cocoa has been grown, the price of cocoa has been steadily declining in real terms for over three decades

- In West Africa, increases in cocoa production, and (real term) decreases in the price of commodity cocoa are NOT the result of new technologies, investments in new trees, scale etc. “Big Chocolate” has been able to squeeze prices through complex trading chains, buffer stocks and a labour situation that can take advantage of cocoa farmers’ poverty. Over 90% of cocoa farmers in West Africa earn an income of less than $1 a day, less than half of what the world bank estimates as a “basic living income”. However cocoa is one of their few ways to earn “cash”, and in some regions – like the Sahel – families are so desperate that they will consider “loaning” or “selling” themselves, and even children, to survive. Ironically, part of the problem here stems from attempts to grow more cocoa in the 1970s when the then President of Cote D’Ivoire, Felix Houphouët-Boigny attracted millions of African farmers to cocoa farmers with generous incentives, including land ownership and citizenship for whoever planted cocoa trees – creating a classic problem of oversupply in labour.

THE CURRENT SPIKE

Unlike e.g. OPEC the cocoa trading boards in the Cote D’Ivoire, Ghana etc. have struggled to control the price of cocoa. Instead the price of cocoa, like most other food “commodities”, (e.g., wheat, rice, sugar, soy, etc.) is set on various international exchanges far from where the commodities are grown. And in the case of cocoa, the key indexes are the New York Mercantile Exchange (NYMEX) and the Intercontinental Exchange (ICE) in London. Over the last year cocoa’s price skyrocketed:

Source: Trading Economics, https://tradingeconomics.com/commodity/cocoa

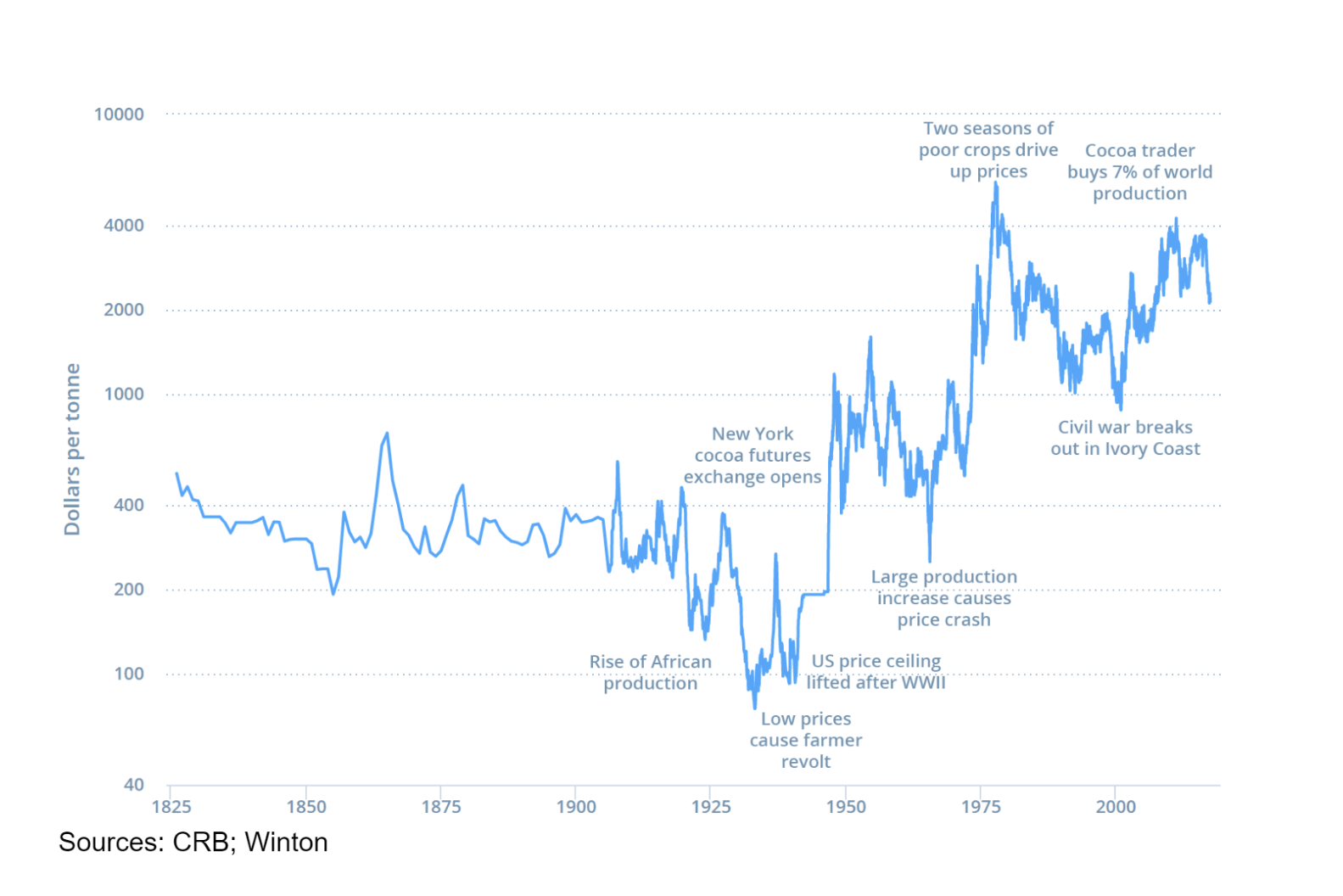

Over the very long term, we’ve seen multiple examples of these spikes – most recently in the early 2000s with a trader nicknamed “ChocoFinger” making a huge upside, and before then in the 1970s when the Cote D’Ivoire tried to set up an OPEC for Cocoa (and ironically the counter measures taken by Big Chocolate then are finally unwinding and may be partly responsible for the current spike, see below)

WHAT’S BEEN CAUSING THE RECENT COCOA PRICE RISE?

The most recent cocoa price spikes have been caused by a “perfect” storm of increasing demand being met with short term supply issues, with the most significant issues being

- War in the Ukraine and also the Middle East – this has disrupted supply chains not just in transporting cocoa, but also in e.g. sourcing fertilisers

- Poor harvests and declining yields – cocoa in West Africa has been hit by a double punch of bad weather and the “breakouts” of two cocoa blights / diseases.

- Over the past few decades, weather conditions have become far more extreme in West Africa, with droughts and torrential rain. And in the last few years, this has been even more severe – for example during the critical cocoa harvesting month of July 2023, Sodexham – the Ivory Coast’s meteorological agency – reported that rainfall that was 20-40% higher that the average of 1991-2000. And this severely damaged crops. At the same time flooding in Q4 2023 meant that many of the roads from the farms to the ports were impassable, so less cocoa could reach the export warehouses.

- The torrential rains have also contributed to the spread of both the black pod disease and the swollen shoot virus in Ghana and Ivory Coast. Late last year the Tropical Research Services reported that approximately 20% of Ghana;s cocoa crop by November was infected by swollen shoot virus.

There are also some longer term, more structural issues. The average farmer in West Africa earns less than $1a day. This has led to the increasingly notorious issue of child, and child slave, labour – as farmers can’t afford to employ more workers, send their kids to school and sometimes even feed them. This poverty has also led to deforestation and underinvestment in “basic” cocoa agriculture. Even though cocoa is their primary cash crop, many farmers literally can’t afford to replant cocoa trees. The last wave of tree planting in West Africa took place in the early 2000s, particularly around the northwest of Ivory Coast. These 20-25 year old trees are well past their prime, and far more prone to diseases and bad weather. Their yields are declining. The ground is less fertile. And this is compounded by poor husbandry, with farmers unable to afford cleaning their cocoa tree roots and preventing the spread of diseases. Without paying farmers more, they can’t afford to plant new trees, care for them, etc. So it’s a vicious cycle. They are condemned to growing commodity cocoa where all they can compete on is price .. and the price is less than they need to live on.

This has led to a significant shortfall in supply. Many experts believe that the cocoa market is heading for its largest shortfall in over 60 years (or possibly ever), with a deficit of 300,000-to-500,000 tons. The latest data showed Ivory Coast farmers shipped 1.12 MMT of cocoa to ports from October 1 to February 18, down -33% from the same time last year. Meanwhile, the Ghana Cocoa Board cut its 2023/24 Ghana cocoa production estimate to a 14-year low of 650,000-700,000 MT from a previous forecast of 850,000 MT.

AN OPPORTUNITY FOR SHORT SELLING

But that’s not all. Back in the 1970’s Président Félix Houphouët-Boigny of the Ivory Coast tried to create an OPEC like structure for West Africa where they could control the price of cocoa by withholding supply via an embargo of cocoa exports, while also dramatically encouraging cocoa farming (offering free land, etc.). For a host of internal reasons this failed – smuggling, internal African politics, etc. Another key reason for this failure was that the big cocoa trading companies put in place MASSIVE inventories of cocoa beans so they could, and did, literally out wait the Cote D’Ivoire’s embargo.

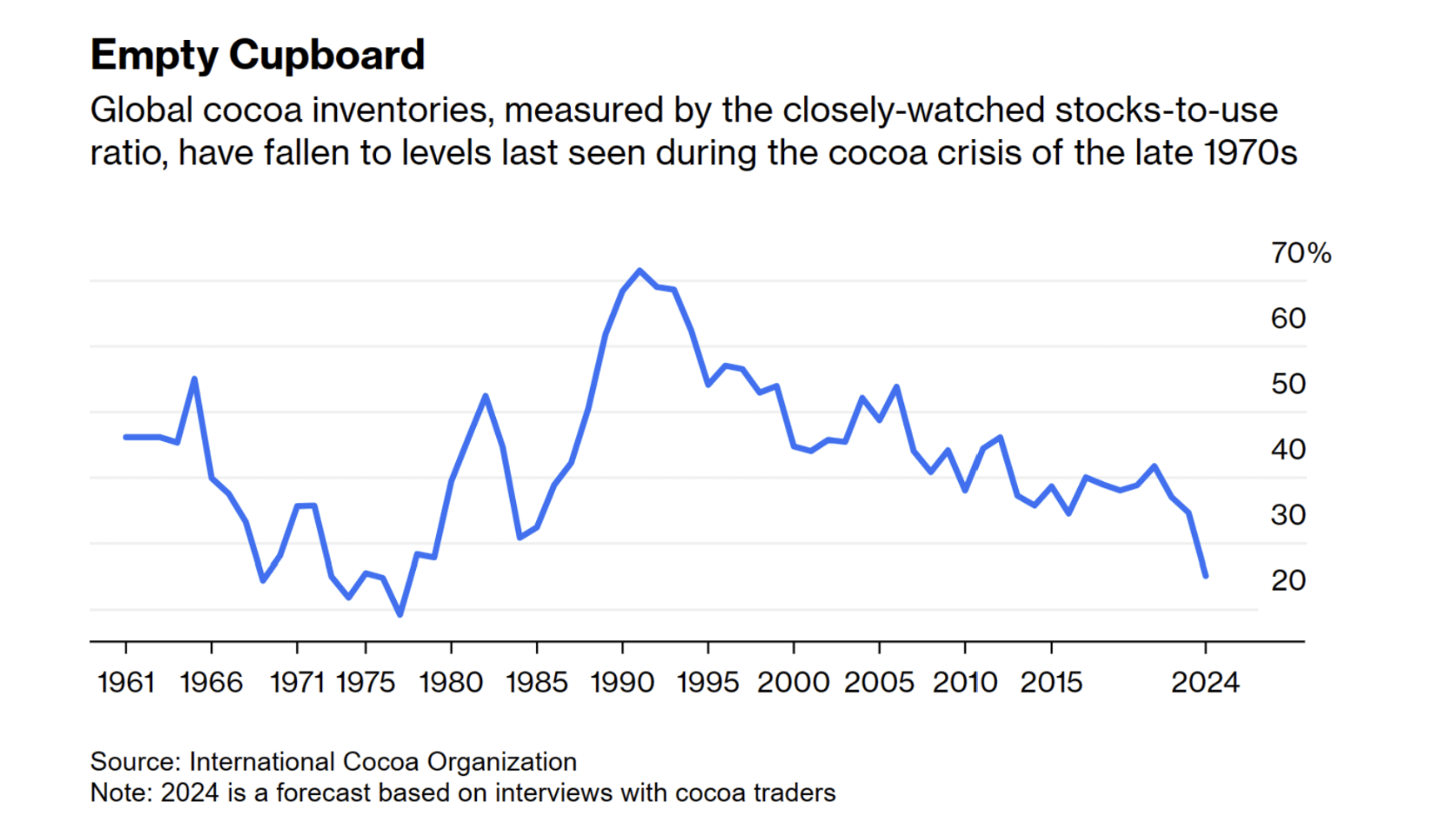

The cocoa trading companies have continued to maintain this “buffer” stock, and it’s “normally” been over 35% of “consumption” needs/ levels. This means that “shorting” cocoa has been pretty tough (although ChocoFinger did manage it in the early 2000s).

But today cocoa stockpiles, measured by the stock-to-consumption ratio, are now forecast to drop to as little as 25%, comparable to the record lows seen in the 1970s when Big Chocolate had to run down stocks to “wait out” the Cote D’Ivoire’s embargo.

This combination of 1) declining supply and 2) reduction in buffer stocks has created a perfect storm. Hedge funds have sensed instability in the market, and piled in. According to a Financial Times investigation this month, a total of $8.7 billion has been poured into the two key British and US cocoa trading platforms, adding more fuel to an already explosive situation.

This has become a classic hedge fund dream play.

IS THIS GOOD NEWS FOR FARMERS?

Short term, there has been some positive news for some farmers. For example, in Ghana late last year the state-guaranteed cocoa price paid to farmers was raised by two thirds from 12,800 cedis 20,943 cedis (US$1,837) per tonne for the upcoming 2023-2024. Cameroon, the world’s fourth-largest cocoa producer, raised the price cocoa farmers get to 1,500 CFA francs (US$2.50) per kilogram, a 25% jump from the previous rate of 1,200 CFA francs. However in the Ivory Coast, where 40% of all cocoa grown comes from, farmers are only seeing a price rise of 10-12%, receiving 1,000 central African francs ($1.63) per a kilogram, about 70-80% below the current wholesale price.

But declining cocoa yields in Ghana, Cameron and the Cote D’Ivoire offset these gains, so their take home income isn’t really that much more (if at all). And even an increase in farmgate prices of 25-70% does not address the structural problem for cocoa farmers where they need $2.50+ as a MINIMUM to live on .. and yet before the recent spike in cocoa prices, they were being paid $.80-.90 (if male) and $0.25-35 (if female). This still isn’t enough for them to break out of the poverty trap, start investing in more cocoa trees, better husbandry, sending their kids to school, etc.

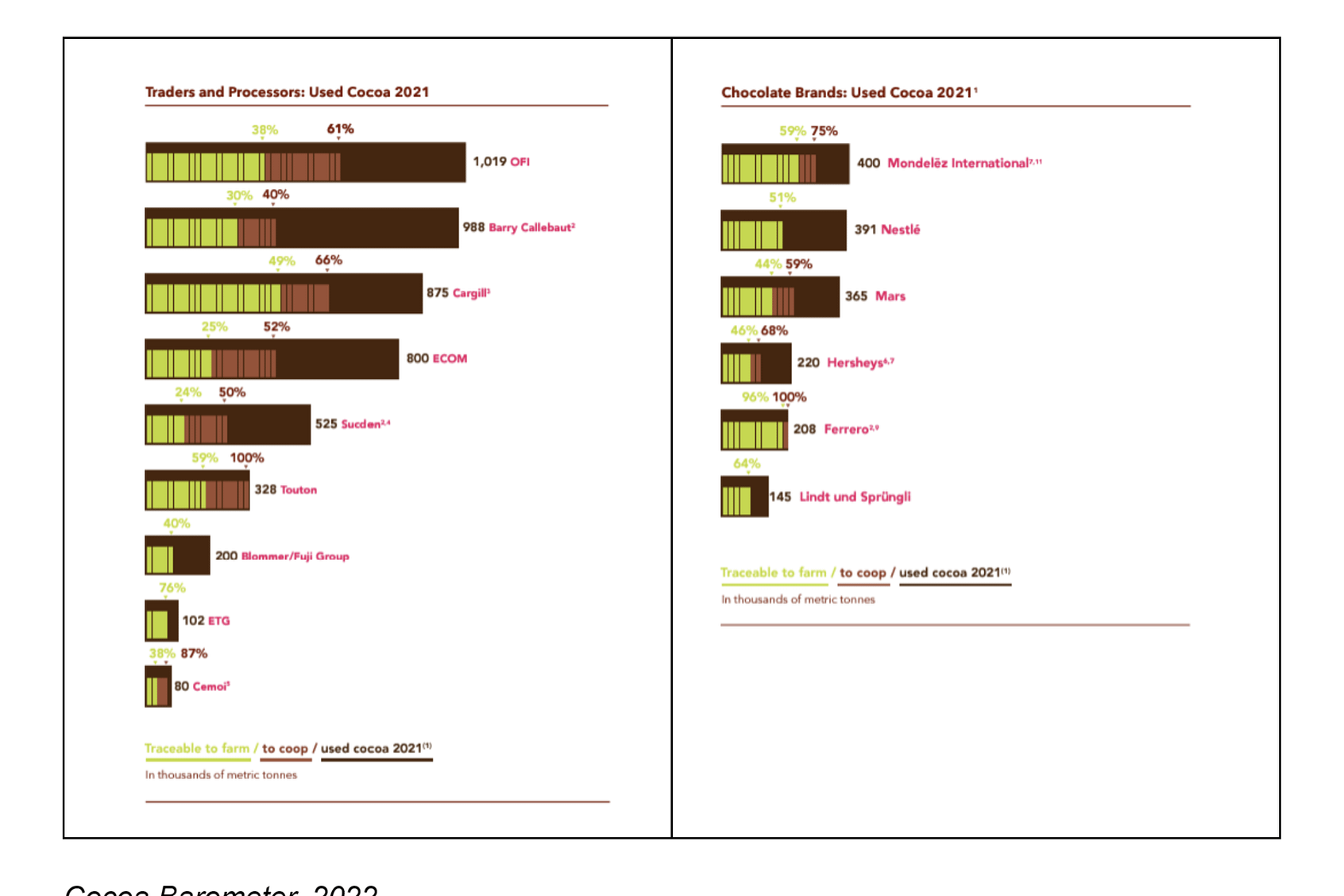

Big Chocolate – both the traders and the big confectionery houses – buy much of their chocolate from small traders. Big Chocolate isn’t concerned about quality (they can add taste, flavour etc. in the factory) and they don’t commit to long term sustainable, transparent and fair contracts with farmers. Unlike craft chocolate, “Big Chocolate” works via small intermediaries – and they don’t know where much / most of their cocoa is coming from. For example, over 50% of Callebaut’s cocoa, until last year the world’s biggest cocoa processor (and key partner of Tony’s), came from “non directly traceable cocoa”.

And it’s these traders, both big and small, who are benefiting the current position. The big traders are taking advantage of the current price spike combined with stock piles from Covid (and forward contracts) to cash out for big profits. The small traders too can enjoy the upside of higher prices. For farmers it’s far harder – their farm gate prices are set by the cocoa trading boards, who aren’t passing on the increase in traded prices, and their yields are down thanks to bad weather and diseases like witches broom and swollen shoots.

MORE BAD NEWS FOR THE CONSUMER OF MASS MARKET CONFECTIONERY

Short term, here are a few more “bad news” predictions from the spike in commodity prices of cocoa for the consumer of mass market bars

- Big Chocolate will use this as ANOTHER excuse to raise prices, on top of the Covid surge prices they’ve already imposed. Just to pick a couple that Sky News pulled together last November for the prior 12 months:

- Asda’s Snack Size Chocolate Caramel Chews increased in price by 107.7%

- Green & Black’s Organic Classic Miniature Chocolate Bar Collection saw a price increase of 67.2%

- Aldi’s Dairyfine Titan and Lidl’s Mister Choc Choco & Caramel Bars (six packs) – both saw similar increases of 75.8% and 66.8% respectively

- Big Chocolate will increasingly use more “CBRs” (cocoa butter replacements) like palm oil, hydrogenated vegetable fats, PGPRs, etc. Note: one silver lining is that the price of sugar has also skyrocketed because of bad harvests / poor weather .. so Big Chocolate may not add in even more sugar .. but it will add in other “stuff” (ie CBRs)

- There will be more “shrinkflation” .. bars will get smaller (again), but hopefully not as much as some of the more egregious examples of a few years ago like or else there really won’t be much left

- Toblerone, owned by Mondelez, reducing the weight of its bars by 25% by adding more space between each piece

- Mars shrinking Maltesers, M&Ms, and Minstrels by up to 15%

- Galaxy chocolate bars being reduced by 10%

THE CHALLENGE FOR CRAFT CHOCOLATE .. PAYING FOR QUALITY

Craft chocolate is built on the belief that consumers will pay more to savour quality bars that are crafted with great beans. Craft chocolate bars do cost more – and craft chocolate makers try to be as transparent as they can, explaining that they pay farmers far more with guaranteed long term contracts at prices that were 3-10X more than the price of commodity cocoa. And this has led to some spectacular successes. In Madagascar we have Bertil Akesson, Menakao and Chocolat Madagascar all paying far higher prices and for the latter two, making in Madagascar too. Elsewhere in Africa, Kokoa Kamili (Tanzania) and Latitude (Uganda) are again inspiring stories whose beans are being used by makers from Norway to Spain to the USA. And craft chocolate has also been key to supporting farmers through South America and the Pacific Rim. In all these farms and co-operatives, new fermentation centres and new drying facilities are being built, new trees are being planted and farmers are being trained how to plant, grow and harvest beans that achieve a significant price premium. And steps are being taken to minimise cocoa’s devastating diseases, protect and replant the rainforest, etc.

However this is all based on the belief that there is a premium to be paid for quality. And as one (anonymised) cocoa grower describes, the current situation is potentially disastrous:

Quality only matters inasmuch as there is something to compare it to at a different value. … The price surge does nothing but hurt quality…farmers have no motivation or incentive to produce quality if there is no differentiation. Right now they can scrape trees for every pod, add stones to sacks, add water to buckets of wet cacao, anything they want … it will be purchased full price no questions asked.

Craft chocolate prices too will have to rise. Perhaps by not as much in percentage terms as mass market confectionery. But we, as consumers, HAVE to support our makers in being will to pay farmers transparently, with long term contracts, a premium for their quality beans.

A SILVER LINING?

There may be a (small) silver lining. And now, more than ever, this price spike means me need to support craft chocolate makers and farmers by paying for quality.

Craft chocolate has always struggled to compete directly with mass market confectionery and snacks where their primary ingredient is sugar. These snacks and vending machine delights rely on the “Bliss Point” to get consumers to scoff more and more. The prices of these bars will dramatically increase. Sugar prices too have spiked following global supply interruptions and from various weather conditions that have led to a series of poor harvests. And there is a limit to how much palm oil, reconstituted vegetable fats, PGPR etc. “big chocolate” can stuff in these snacks.

So MAYBE consumers will finally realise that the costs of eating these UPF chocolate snacks isn’t good value. Personally I doubt this. But it’d be great for their pockets, their (and the nation’s) health and the farmers.

More interesting is the impact on the “wannabe” health and ethical bars that supermarkets and big brands are trying to sell. These are the bars where they claim to be single “origin” but don’t say the farm or co-op. These are the bars with “simple ingredients”, which look “clean” .. but they don’t tell you how, or where, they’ve actually been made (for more on this, and why they too are almost always “ultra processed”, please see here). For these bars, cocoa is a key ingredient (even if the way it’s been ultra processed destroys much of cocoa’s antioxidants, flavonoids, and indeed flavour overall). And as the price of these currently £2-3 bars increases, craft chocolate will have a chance to attract more consumers. And once they do, consumers will hopefully realise that it’s worth paying a bit more for a VASTLY healthier and more flavoursome experience.

CRAFT CHOCOLATE AND PRICES

At some point we will have to raise the prices of some of our bars (and we’ve already raised a few). Hopefully this will be less than the 20-30% prices seen already since Covid in many confectionery bars. But part of our promise, and the reason why we believe in craft chocolate, is that we want to support the farmers, co-operatives and makers. We don’t want to be like Big Chocolate where they mercilessly squeeze their supply chains. So we’re going to have to continue to raise prices accordingly (and yes, Brexit has made importing a LOT, LOT more expensive – both in terms of paperwork, logistics costs and import duties).

For now and at least the next 6 months we’re going to keep the price of our subscription boxes at £22.95 (plus P&P) for current subscribers which really does represent incredible value. But we will have to raise it for new subscribers in a few months (so hurry up and subscribe if you want to lock in the current price).

And please no rotten (ie ultra processed) eggs this Easter!

PS I’ve also just a podcast with “The Food Fight” where we discuss a few of these issues, and much more too! See HERE

SOURCES

https://www.forbes.com/sites/christinero/2023/01/03/balancing-power-in-cocoa-by-paying-farmers-more/?sh=3738f0b169a2

https://tradingeconomics.com/commodity/cocoa

https://www.ucl.ac.uk/news/2023/oct/analysis-cocoa-prices-are-surging-west-african-countries-should-negotiate-better-deal

https://corpaccountabilitylab.org/west-africa-cocoa-report-2023

https://news.sky.com/story/which-festive-chocolates-have-gone-up-by-more-than-60-13036710

https://www.foodmanufacture.co.uk/Article/2023/11/08/Avoiding-disruption-as-cocoa-and-sugar-prices-rise

https://www.fao.org/3/y4343e/y4343e05.htm

https://www.confectioneryproduction.com/news/47294/cocoa-prices-hit-fresh-stock-exchange-highs-as-pressure-on-global-markets-continues/

https://time.com/5671166/ghana-cocoa-trees-swollen-shoot-disease/

https://www.winton.com/news/cocoas-bittersweet-bounty-200-years-in-charts